Yes, insurance will pay for a new roof when the damage results from covered perils like storms, hail, or wind. However, the amount you receive depends heavily on your policy type and the insurance adjuster’s assessment of the damage.

Your homeowners insurance typically covers sudden, accidental roof damage but excludes wear and tear or maintenance issues. The key factors that determine coverage include the cause of damage, your specific policy terms, and whether you have Actual Cash Value or Replacement Cost Value coverage.

Key Insight: Most insurance companies will only cover roof replacement when damage exceeds a certain threshold, usually requiring multiple damaged areas or structural compromise rather than isolated shingle loss.

Understanding these coverage rules before you need them can save you thousands of dollars and prevent claim surprises when storm damage strikes your Rocky River or Cleveland area home.

When will insurance cover your roof replacement?

Insurance companies cover roof replacement when damage stems from what they call “covered perils.” These include wind damage from storms that tear off shingles or compromise roof structure, hail impacts that crack or break roofing materials, and fallen trees or branches during severe weather.

Fire damage, including lightning strikes, also qualifies for coverage, as does structural damage from excessive ice, snow, or sleet accumulation. In Northeast Ohio, where we experience harsh winters and severe thunderstorms, these weather-related damages are particularly common. Vandalism and malicious damage by others round out the typical covered events.

What insurance won’t cover is equally important to understand. Normal wear and tear, gradual deterioration, poor maintenance, and age-related failure don’t qualify. If your 20-year-old shingles are simply reaching the end of their useful life, you’ll pay for replacement yourself.

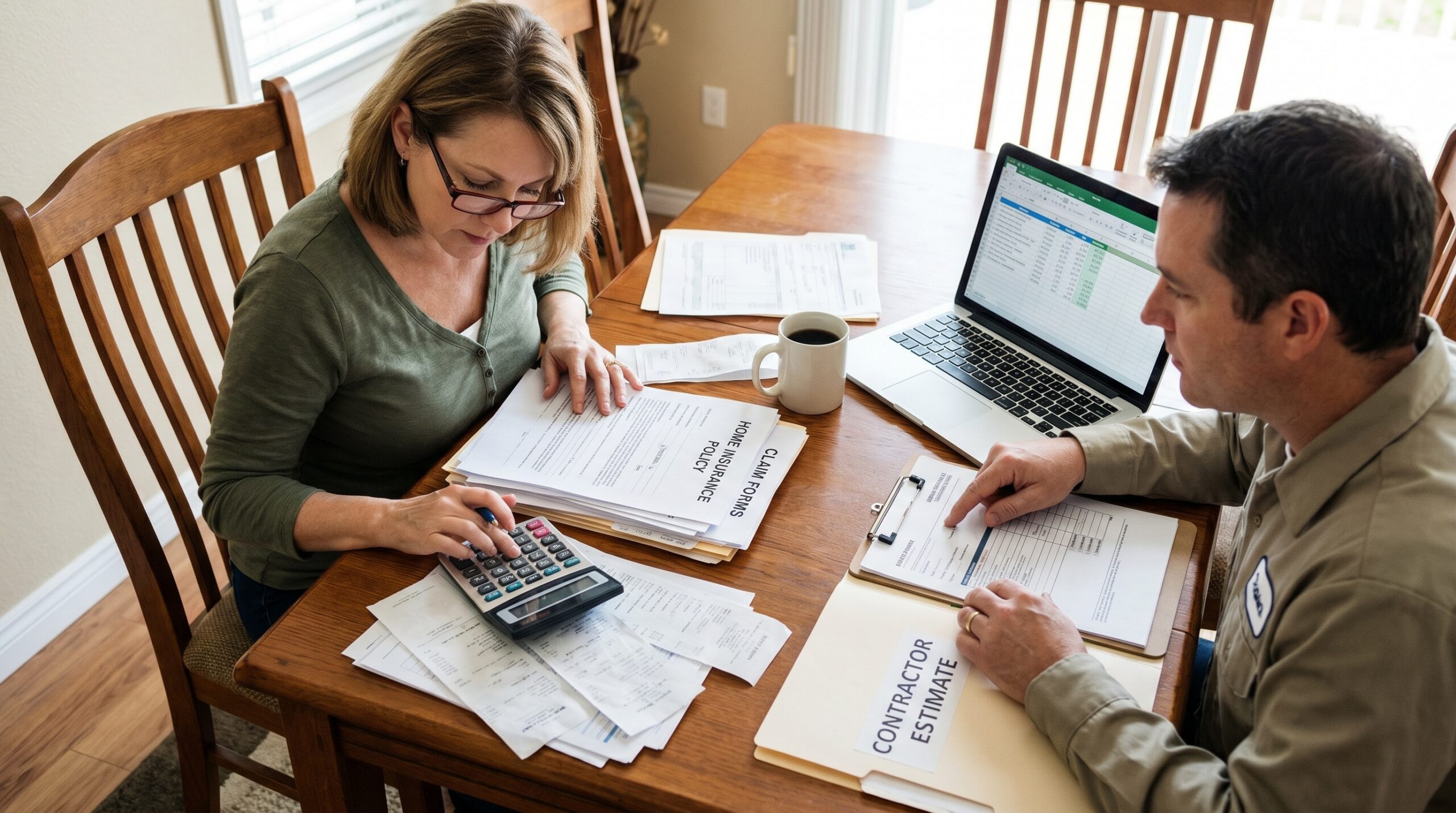

The insurance adjuster holds the final decision on whether damage warrants full replacement or just repairs. They evaluate the extent of damage, structural integrity, and whether repairs can restore your roof to its pre-loss condition. Working with experienced local roofing contractors who understand insurance restoration can help ensure proper documentation of storm damage.

How your policy type affects the payout amount

Your insurance policy type dramatically impacts how much money you receive for roof replacement. The two main types are Actual Cash Value and Replacement Cost Value, and the difference can mean thousands of dollars out of your pocket.

| Policy Type | Coverage Amount | Payment Method | Your Cost |

|---|---|---|---|

| Actual Cash Value (ACV) | Depreciated roof value | Single payment | Deductible + depreciation gap |

| Replacement Cost Value (RCV) | Full replacement cost | Two payments | Deductible only |

An Actual Cash Value policy pays only the depreciated value of your roof at the time of loss. If your roof cost $15,000 to install 10 years ago but is now worth only $8,000 due to age, that’s all you’ll receive minus your deductible. You’ll cover the remaining replacement cost yourself.

Replacement Cost Value policies pay the full cost to replace your roof with similar materials at current prices. You’ll receive an initial payment for the actual cash value, then a second payment for the recoverable depreciation after you complete the work and submit proof.

Important Note: Even with RCV coverage, insurance only pays to restore your roof to its original condition. Upgrades like switching from basic shingles to premium materials come out of your pocket.

Do you still pay your deductible?

You must pay your deductible regardless of the claim amount or circumstances. This is non-negotiable, despite what some roofing contractors might suggest.

Your deductible applies before insurance pays anything on an approved claim. If you have a $2,500 deductible and a $12,000 roof replacement, you pay $2,500 and insurance covers the remaining $9,500 (assuming RCV coverage).

Some contractors offer to “waive” or “absorb” your deductible, but this practice constitutes insurance fraud. These contractors typically inflate their estimates to cover the deductible cost, which violates your insurance contract and can lead to claim denial or legal consequences.

Wind and hail deductibles in storm-prone areas often differ from your standard deductible. These specialized deductibles are typically percentage-based rather than flat dollar amounts, potentially costing you more during severe weather events.

What if your insurance estimate is too low?

Insurance estimates frequently fall short of actual replacement costs due to outdated pricing, missed line items, or conservative labor calculations. When this happens, you have several options to bridge the gap.

Supplementing your claim involves documenting additional costs and submitting them to your insurance company for review. This process requires detailed evidence of why the original estimate was insufficient, including contractor assessments and current material pricing.

Working with experienced local contractors who specialize in insurance restoration often yields better results than handling supplementation alone. Insurance companies typically respond more favorably to requests from policyholders rather than contractors, but professional support helps ensure you include all necessary details. Local roofing experts familiar with Northeast Ohio weather patterns and insurance practices can provide valuable guidance throughout the claims process.

If supplementation doesn’t work or seems too time-intensive, you can use the insurance payout to cover most costs and pay the difference yourself. Many homeowners in the Rocky River and Cleveland area choose this route when the gap is manageable and they want to avoid claim delays.

Financing your roof replacement offers another solution, allowing you to complete the work immediately while making monthly payments. This approach lets you use insurance money as a down payment while spreading the remaining cost over time.

Pro Tip: Get multiple contractor estimates before filing your claim to understand the true replacement cost and potential insurance shortfall in your area.

The insurance claim process can feel overwhelming, but understanding your coverage limits and options helps you make informed decisions. Whether your claim gets approved for the full amount or requires additional steps, knowing these fundamentals puts you in control of the situation.

Remember that insurance companies exist to restore your property to its pre-loss condition, not to provide upgrades or cover maintenance issues. Setting realistic expectations and understanding your policy details before damage occurs gives you the best chance of a smooth claim experience when you need it most. For Rocky River and Northeast Ohio homeowners, working with local roofing professionals who understand both the regional weather challenges and insurance restoration process can make all the difference in achieving a successful outcome.