When you need a new roof in Northeast Ohio, the price tag can feel overwhelming. Most Cleveland-area homeowners face costs between $9,000 and $25,000 depending on your home’s size and material choices. If you live in Rocky River, Westlake, or Cleveland Heights, paying that amount upfront might not fit your monthly budget.

The good news is you have multiple financing paths to get the roof you need now while managing your cash flow. From contractor financing with promotional rates to home equity loans with competitive terms, Ohio homeowners can choose options that match their financial situation and timeline.

Quick Answer: Ohio homeowners can finance roof replacements through contractor financing (fastest approval), personal loans (no collateral), home equity products (lowest rates), or local heritage assistance programs. Most options offer terms from 12 months to 20 years with rates varying by credit score and loan type.

This guide walks you through each financing option, what questions to ask before signing, and how 2026 tax credits might apply to your Ohio roofing project.

Understanding your roof financing mindset in the Midwest

Before diving into specific loan products, think about what matters most for your situation. Financing isn’t just about getting approved—it’s about balancing four key factors that will impact your experience during Ohio’s unpredictable construction seasons.

First, consider your monthly payment comfort zone. A lower payment might mean paying more interest over time, but it could also preserve your emergency fund for other home repairs. Second, look at total cost including interest and fees. A 0% promotional offer might cost more than a standard loan if you can’t pay it off before the Ohio winter sets in.

Speed matters too, especially if you’re dealing with active leaks from lake-effect snow or storm damage. Some financing options can get you approved and scheduled within days, while others might take weeks. Finally, think about flexibility—do you want the option to pay extra or refinance later without penalties?

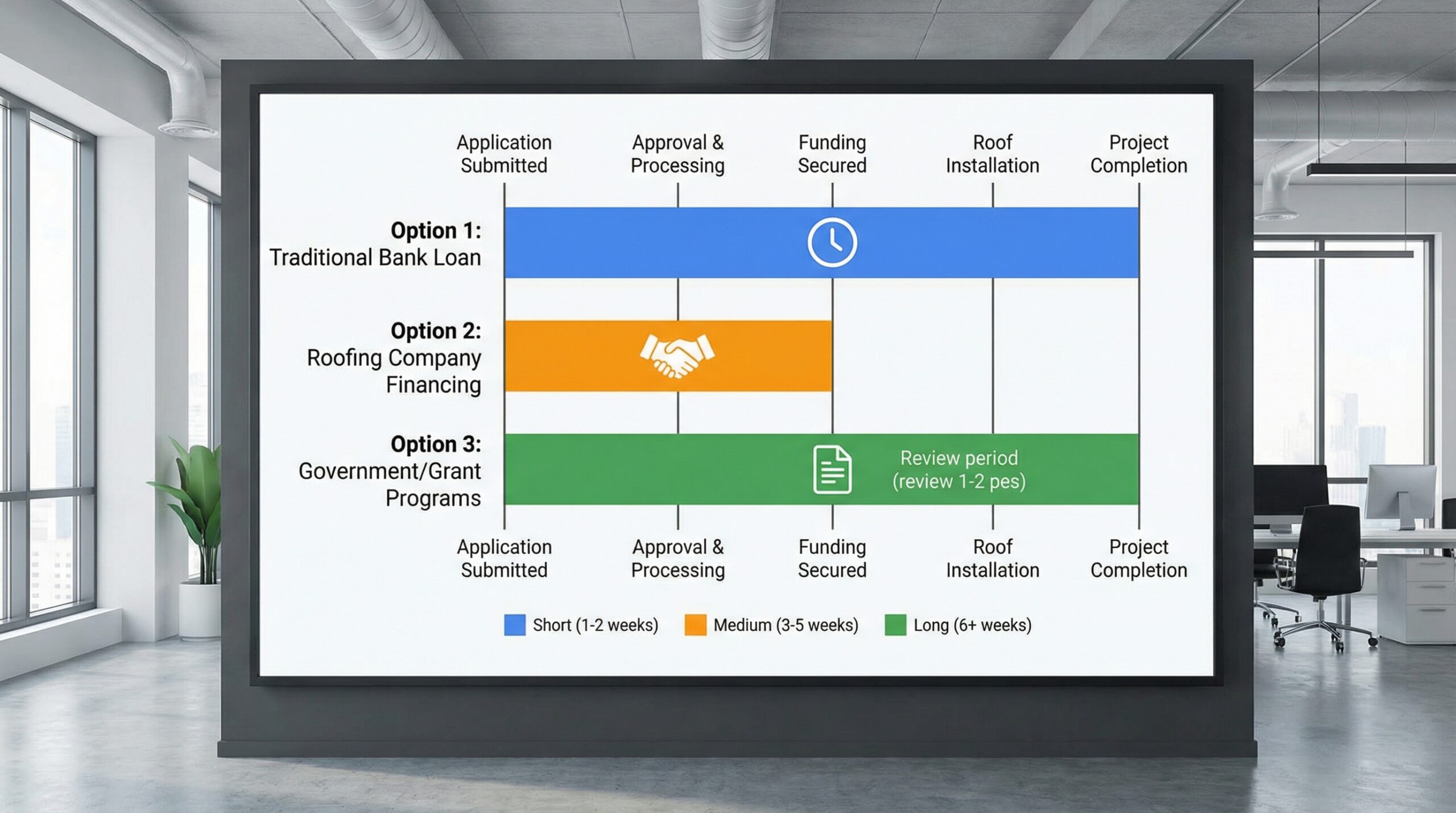

Contractor financing for speed and convenience

Many Northeast Ohio homeowners choose contractor financing because it streamlines the entire process. You can get approved, select materials, and schedule installation all in one conversation. This option works particularly well when you need repairs quickly due to spring hail storms or active winter leaks.

Peak and Valley Roofing partners with leading lenders to offer flexible terms. Common structures include deferred payment periods, promotional low-interest rates, and longer-term fixed payments with competitive rates tailored for the Cleveland market.

Before signing any contractor financing agreement, ask these critical questions. Is the interest rate promotional, and what happens when that period ends? Many offers include deferred interest clauses where interest accrues during the promotional period and gets charged if you don’t pay off the balance in time. Also confirm any origination fees, closing costs, or prepayment penalties. Understanding what should be included in a detailed roofing estimate can help you evaluate the total project cost before committing.

Important Note: Contractor financing with 0% promotional rates can be excellent tools if you have a clear payoff plan. Divide your total amount by the promotional months and aim to pay that amount monthly to avoid surprise interest charges.

This financing path works best for homeowners who value speed and simplicity, especially when dealing with urgent repairs that can’t wait for traditional bank processing.

Personal loans and home equity options in Ohio

Personal loans offer a middle ground for Ohio homeowners who want financing without using their home as collateral. These unsecured loans typically range from 2 to 7 years with fixed monthly payments that make budgeting predictable for the 2026 season.

The main advantage is speed and simplicity—no home appraisal or lengthy underwriting process. However, rates tend to be higher than secured options because lenders take on more risk. Your credit score and income heavily influence both approval and the interest rate you’ll receive from local Ohio banks or national lenders.

Home equity loans and HELOCs (Home Equity Lines of Credit) often provide the lowest interest rates because your home secures the loan. A home equity loan gives you a fixed amount with predictable payments, while a HELOC works like a credit line with variable rates—useful if you’re also planning siding or gutter work.

Ohio homeowners with bad credit still have options through specialized lenders, though rates will be higher. Some contractors work with lenders who focus on home improvement loans for lower credit scores, making roof replacement accessible even when traditional financing isn’t available.

The trade-off with home equity products is time and complexity. You’ll need an appraisal, more documentation, and potentially closing costs. But for larger projects in areas like Shaker Heights or Westlake, the lower rates can save thousands over the loan term.

Ohio assistance programs and 2026 tax considerations

Northeast Ohio offers unique programs that can help qualifying homeowners. The **Heritage Home Program**, available in many Cleveland suburbs, provides technical advice and access to low-interest fixed-rate loans for homeowners of houses over 50 years old. These loans can be used for roof repair and replacement while preserving the historic character of your home.

Additionally, local community development blocks in cities like Lakewood often provide emergency repair grants or low-interest loans for income-qualified households. These programs typically focus on households at or below 80% of Area Median Income and help address critical safety issues like failing roofs.

For 2026 tax considerations, standard asphalt shingles typically don’t qualify for federal energy tax credits. However, if you’re adding energy-efficient improvements like qualifying attic insulation or solar shingles (like GAF Energy’s Timberline Solar) as part of your project, you might be eligible for significant credits.

The federal solar credit can apply to integrated solar roofing systems, while Section 25C credits may cover qualifying attic insulation or ENERGY STAR skylights installed during the project. Always keep detailed invoices and confirm eligibility with an Ohio tax professional.

| Financing Option | Typical Terms | Best For | Key Considerations |

|---|---|---|---|

| Contractor Financing | 12-120 months | Speed, convenience | Check 0% promo details |

| Personal Loan | 2-7 years | No collateral needed | Credit score dependent |

| Home Equity / HELOC | 10-20 years | Lowest rates | Longer approval time |

| Heritage Home Program | Fixed low-rate | Homes 50+ years old | Specific to participating cities |

Making your financing decision

Choosing the right financing option depends on your specific situation, but a few key steps can help you make the best decision. Start by determining your comfortable monthly payment range and gathering quotes from local Ohio contractors with detailed, line-item estimates.

Compare financing offers using APR rather than just interest rates, since APR includes fees and gives you the true cost of borrowing. Ask about ventilation and flashing details in your roofing scope, as these are common areas where problems develop if not properly addressed. Understanding the essential components of roof flashing can help you evaluate whether your contractor’s proposal includes proper Midwestern installation techniques.

If you’re considering any tax credits, confirm eligibility requirements before making material selections. Some energy-efficient products have specific certification requirements that must be met to qualify for credits. When evaluating your options, it’s also worth exploring different roofing materials and their long-term value, as choosing the right material can impact your total cost of ownership.

For Ohio homeowners interested in premium materials, learning about copper roofing and flashing options can help you understand whether these durable materials justify their higher initial investment when factoring in financing costs.

The most important thing is getting a roof that protects your home while fitting your budget. Whether you choose fast contractor financing, low-rate home equity options, or local Ohio assistance programs, the right financing makes it possible to address your roofing needs without compromising your financial stability.

Remember that your roof is a long-term investment in your home’s protection and value. Taking time to understand your financing options ensures you get both the quality roof and payment structure that work best for your situation. Consider reviewing roof lifespan by material to understand how your choice affects the total cost of ownership over time.