When your roof gets damaged by hail and your insurance approves the claim, you might receive an initial payment that seems lower than expected. The missing amount is often recoverable depreciation, money your insurer withholds until repairs are completed. But who actually gets this second check when it arrives?

The homeowner typically receives the recoverable depreciation check, as they are the policyholder entitled to insurance benefits. However, the check may be made out to multiple parties including the contractor, mortgage company, or both depending on your policy terms and repair contracts. Understanding this process helps Cleveland and Northeast Ohio homeowners avoid confusion and ensures you receive all the money you’re owed.

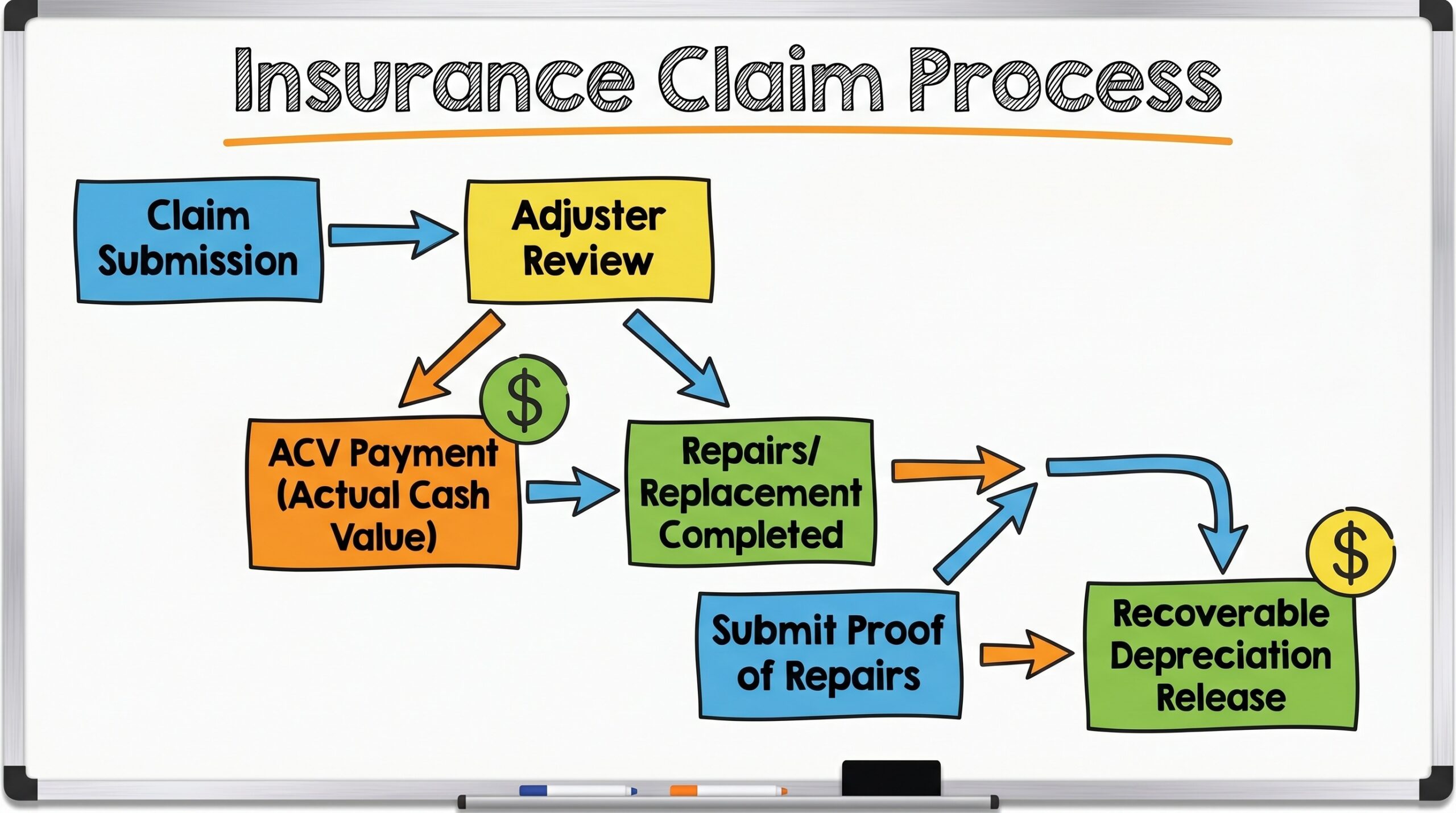

Key Point: Recoverable depreciation represents the difference between your property’s depreciated value and the full replacement cost. You must complete repairs and submit proof to receive this money.

What is recoverable depreciation in insurance claims

Recoverable depreciation is the portion of your insurance payout that accounts for your property’s age and wear. When you file a claim, your insurer calculates two values: the actual cash value (what your damaged property was worth before the loss) and the replacement cost value (what it costs to replace it new).

The gap between these amounts is depreciation. Under replacement cost coverage, this depreciation becomes “recoverable” once you complete the repairs. For example, if your 10-year-old roof costs $20,000 to replace but has $5,000 in depreciation, you’ll initially receive $15,000. The remaining $5,000 becomes available after you finish the work and submit documentation.

Your insurance estimate will show line items like “less recoverable depreciation” and “net claim remaining if depreciation is recovered.” These terms indicate money you can claim back later, not funds you’ve lost permanently.

How the recoverable depreciation payment process works

The payment process typically happens in two stages. First, your insurance company issues an actual cash value payment after approving your claim. This covers the depreciated value of your damaged property minus your deductible.

Second, after you complete repairs and submit proof, the insurer releases the recoverable depreciation. This proof usually includes final invoices from your contractor, photos of completed work, and sometimes a completion certificate. The timeline for submitting this documentation varies by policy but commonly ranges from six months to two years.

Important: Missing the deadline to submit completion proof means you forfeit the recoverable depreciation permanently, even though you paid premiums for replacement cost coverage.

Most policies require you to actually spend money on repairs, not just get estimates. Simply hiring a contractor isn’t enough – you need to show the work is finished and paid for. Some insurers accept signed contracts for large projects like roof replacements, allowing you to receive depreciation before completion.

Who keeps the recoverable depreciation check

The policyholder (homeowner) is legally entitled to recoverable depreciation funds, but the check’s payee line determines who can cash it. Insurance companies typically make checks payable to the homeowner alone, the homeowner and mortgage company jointly, or sometimes include the contractor as a co-payee.

When you’re the sole payee, you control the funds completely. You can deposit the check and pay your contractor according to your agreement. If your mortgage company is listed, they must endorse the check before you can access the money, which can add processing time.

| Check Payee | Who Endorses | Payment Control | Common Scenario |

|---|---|---|---|

| Homeowner only | Homeowner | Full control | No mortgage or small claims |

| Homeowner + Mortgage Co. | Both parties | Shared control | Mortgaged property |

| Homeowner + Contractor | Both parties | Shared control | Assignment of benefits |

Some contractors request assignment of benefits, making them co-payees on insurance checks. While this can streamline the process, it also means you share control of the funds. Make sure you understand any agreements before signing them.

Does recoverable depreciation go to the contractor or homeowner

Recoverable depreciation belongs to the homeowner as the policyholder, regardless of who performs the repairs. However, contractual agreements between you and your contractor can affect how these funds are handled in practice.

Many homeowners choose to endorse recoverable depreciation checks directly to their contractor as payment for completed work. This is perfectly legal and often convenient, but it’s your choice to make. The contractor doesn’t automatically have rights to these funds unless you’ve signed specific agreements.

Some contractors offer to handle the entire insurance process, including collecting depreciation on your behalf. While this can reduce your administrative burden, make sure you understand the terms. You should always receive copies of all insurance correspondence and maintain oversight of the claim process.

The key is transparency. Whether you pay the contractor from your own account after receiving the depreciation check, or endorse it directly to them, both approaches are common and acceptable. What matters is that you understand and agree to the arrangement beforehand.

Working with experienced local contractors who specialize in insurance restoration can help ensure proper documentation and timely submission of completion proof, maximizing your chances of receiving all recoverable depreciation you’re entitled to. Professional roofing contractors in the Cleveland area understand insurance requirements and can guide you through the process while maintaining clear communication about fund handling.

Understanding who gets the recoverable depreciation check helps you make informed decisions about your insurance claim. Remember that these funds are part of your policy benefits – money you’ve paid premiums to access. Whether you receive the check directly or arrange for it to go to your contractor, the important thing is completing your repairs properly and submitting the required documentation on time.